Timber Demand

A combination of increasing demand and static output from forests is likely to lead to a long term increase in timber prices. Growth of the renewable energy market has increased demand for woody biomass for heat and power generation and this demand is now well established within the UK timber supply-chain.

Timber Market

Forestry is an established market and therefore allows investors to choose between age class which will dictate the level of capital appreciation and dividend returns over a defined time period. This also affords investors the choice of when to liquidate their investment to suit their cash flow requirements.

Timber Imports and Growth

Data from Forest Industries Ireland and Central Statistics Office shows that Ireland remains a net importer of timber and wood products in 2025, despite growth in its domestic forestry sector. Annual wood product imports are valued at over €1.5 billion, reflecting strong demand from the construction and housing sectors. While Ireland produces significant volumes of softwood, particularly Sitka spruce, it still relies heavily on imports for hardwood and wood-based panels such as plywood and MDF. Domestic roundwood production is approximately 4–4.5 million cubic metres per year, below long-term targets. Continued low afforestation rates have limited supply growth, meaning imports remain essential to meet rising demand for sustainable building materials.

Future Demand

A combination of increasing demand and static output from forests is likely to lead to a long term increase in timber prices. Growth of the renewable energy market has increased demand for woody biomass for heat and power generation and this demand is now well established within the UK and Irish timber supply-chains.

Supply Constraints

The EU timber Regulation 2013 and the US Lacey Act designates that the importation of timber can originate only from sustainable and traceable sources. It is estimated that approximately 20% of the current global round-wood harvest is via illegal logging.

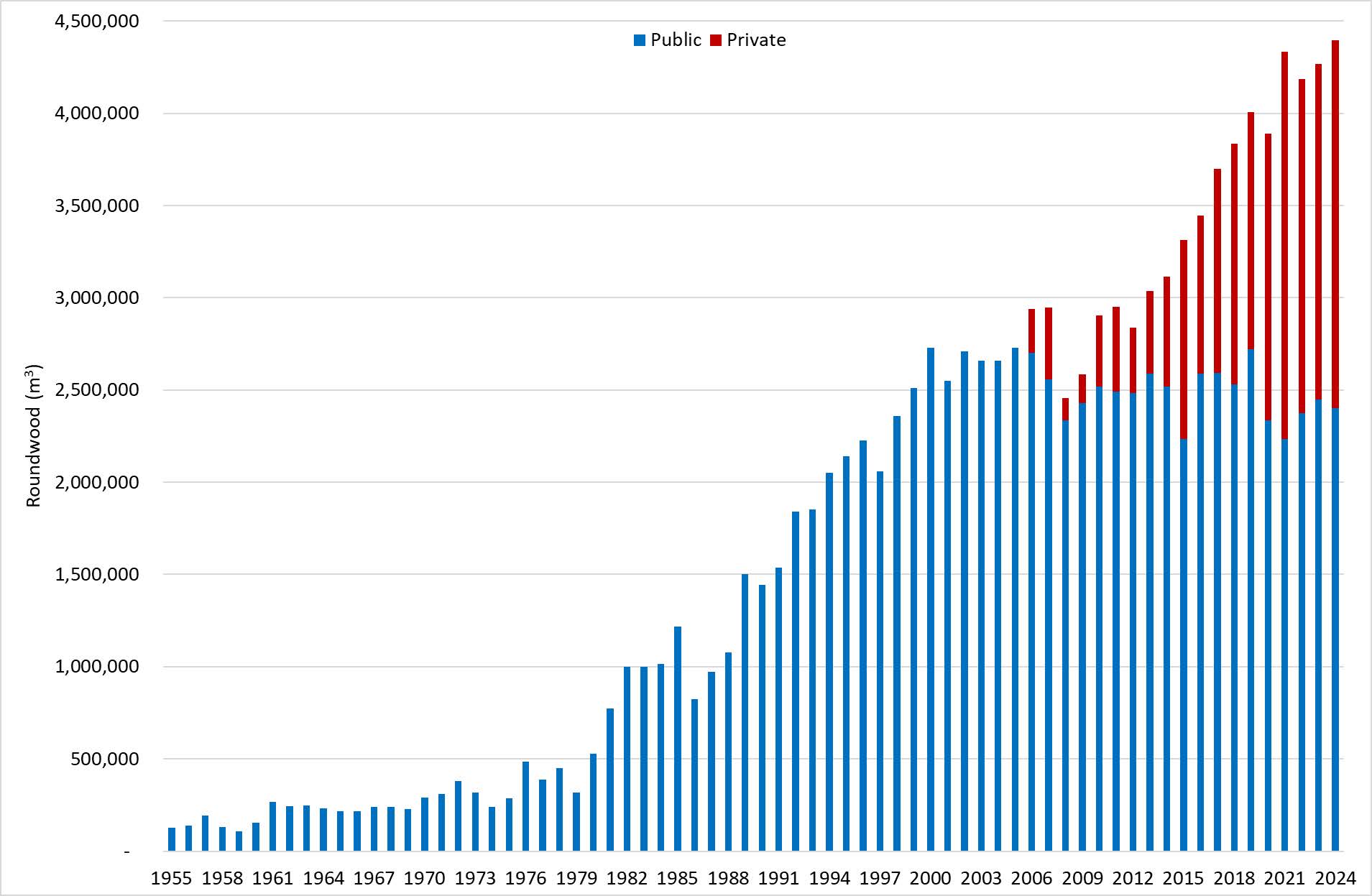

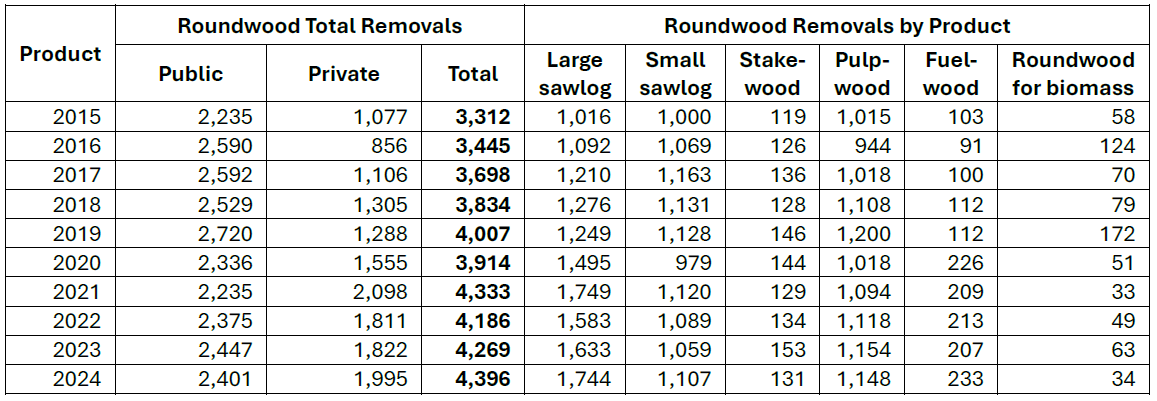

Irish forests continue to supply increasing amounts of wood fibre for sawmilling, panel board mills and the wood energy markets. The annual potential roundwood supply will increase from 4.7 million cubic metres in 2021 to 7.9 million cubic metres by 2035 (COFORD, 2021). This will be followed by a small decrease to remain constant at circa 7.6 million cubic metres up to 2040. Realising this large increase in potential production will entail significant capital investment in roads, harvesting equipment and wood processing. The Irish sawmilling sector is well placed to process this increased production in supply, with many products exported to markets in the United Kingdom and further afield.

Republic of Ireland. Much of this increase came from the private sector roundwood production with an 85% increase in 2024 production compared to 2015. This is reflective of the maturing private forest estate. Non-coniferous removals are still a minor element of the annual roundwood available for processing, and in 2024 amounted to 26,000 m3. Between 2015 and 2024, non coniferous removals averaged 18,400 m³. Storms Darragh and Eowyn will likely increase the roundwood removals for 2025.